Case Study Highlights

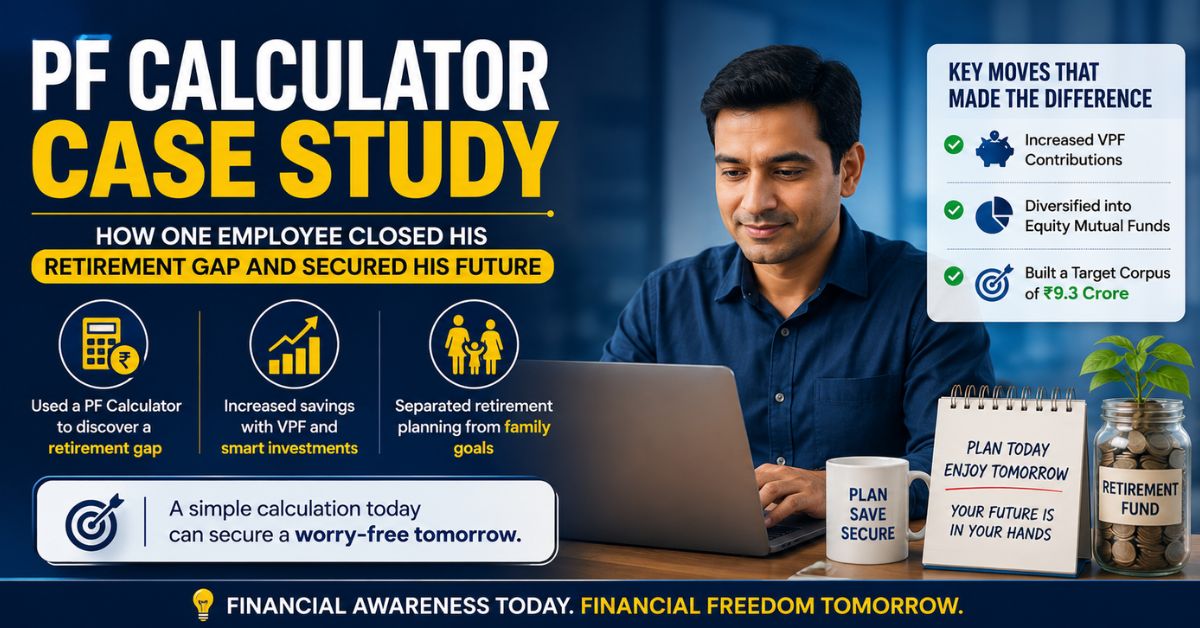

- A 35-year-old salaried employee discovered a major retirement gap after using a PF calculator.

- Inflation-adjusted projections showed EPF savings alone would not sustain his future lifestyle.

- The employee increased retirement contributions through VPF and diversified into equity mutual funds.

- The PF calculator helped separate retirement planning from family goals like education and marriage.

- The case highlights how financial calculators can trigger practical long-term planning decisions.

Retirement planning in India often begins with assumptions rather than calculations. For many salaried employees, the Employee Provident Fund is treated as an automatic savings mechanism that quietly grows in the background over decades. Since contributions are deducted directly from salary, the existence of a PF balance itself creates a sense of financial security.

In reality, however, retirement adequacy depends less on the existence of savings and more on whether those savings can sustain future purchasing power. Inflation, lifestyle expansion, healthcare costs, and dependent responsibilities significantly alter what a “comfortable retirement” actually requires.

This case study examines how one salaried professional used an EPF Calculator to reassess his long-term financial position and restructure his retirement strategy while there was still enough time to course-correct.

The identity of the individual has been partially anonymized for privacy purposes, but the financial patterns, calculations, and planning decisions reflect a realistic middle-to-upper-middle-class salaried household in urban India.

Background Profile

The subject of this case study is Mr. Abhishek Patel, a 35-year-old salaried employee based in Navsari, Gujarat.

In 2022, Abhishek was working in a senior operations role at a private manufacturing company with a monthly salary of approximately ₹1,50,000. His compensation structure included standard EPF deductions under the Employees’ Provident Fund scheme, along with employer contributions.

Like many working professionals in his income bracket, Abhishek believed he had started retirement planning relatively early. His assumptions were built around three common beliefs among salaried employees:

- EPF contributions over 25 years naturally become “large enough.”

- Regular salary hikes eventually solve long-term wealth accumulation.

- Retirement planning can be postponed until the 40s.

At the time, his financial priorities were largely focused on present-day stability. He had recently purchased a house through a home loan, was managing school expenses for his daughter, and maintained moderate SIP investments in mutual funds. His PF account was viewed as a stable retirement pillar that required little active management.

Importantly, Abhishek had never attempted to estimate the actual cost of his future lifestyle after retirement.

That changed after he used a PF and retirement corpus calculator during a workplace financial literacy session conducted by an external advisor.

The Trigger: From Assumption to Numerical Reality

The calculator exercise initially appeared routine. Employees were asked to input basic information including:

- Current age

- Existing PF balance

- Monthly basic salary

- Employee and employer contribution percentages

- Expected annual salary hikes

- Retirement age

- Inflation assumptions

Abhishek entered the following assumptions into the calculator:

| Parameter | Input Value |

|---|---|

| Current Age | 35 Years |

| Retirement Age | 60 Years |

| Monthly Salary | ₹1,50,000 |

| Annual Salary Growth | 8% |

| Expected EPF Return | 8.1% |

| Inflation Assumption | 6.5% |

At first glance, the projected PF corpus appeared substantial. The calculator estimated that his EPF and related contributions could potentially grow into several crores by retirement.

However, the second stage of the analysis introduced inflation-adjusted retirement income projections.

This was the turning point.

The calculator demonstrated that the purchasing power of ₹1.5 lakh per month in 2022 would be significantly lower after 25 years of inflation. Even conservative assumptions showed that maintaining the same lifestyle in retirement would require a dramatically larger monthly income than he had anticipated.

The projection highlighted a retirement gap between expected PF accumulation and estimated retirement needs.

In simple terms, Abhishek realized that while his PF corpus looked “large” numerically, it was insufficient relative to future expenses.

Understanding the Retirement Gap

One of the most common mistakes in retirement planning is confusing nominal wealth with real wealth.

A corpus of ₹3 crore or ₹4 crore may appear financially comfortable in present-day terms. However, inflation steadily erodes purchasing power over long periods. Expenses such as healthcare, housing maintenance, travel, insurance, and family support tend to rise faster than average inflation.

The PF calculator visualized this effect clearly.

Using inflation-adjusted estimates, Abhishek discovered that his projected retirement income would likely fall short of sustaining:

- His current standard of living

- Future healthcare expenses

- Financial support for dependents

- Emergency liquidity requirements

- Lifestyle flexibility after retirement

The realization was psychological as much as mathematical.

Until that point, his financial planning was based on accumulation. The calculator shifted his thinking toward sustainability.

He later described the exercise as the first time he understood the difference between “saving money” and “planning retirement.”

The Immediate Strategic Changes

Within months of reviewing the projections, Abhishek began restructuring his financial strategy. Instead of treating PF as a passive retirement instrument, he started viewing it as one component within a broader allocation framework.

The changes he implemented were practical rather than aggressive.

1. Increasing Contributions Through VPF

The first decision involved increasing his retirement savings rate through the Voluntary Provident Fund.

Under VPF, employees can contribute beyond the mandatory 12% EPF deduction while continuing to receive similar interest benefits. Since the contributions are salary-linked and automated, the structure also reduces behavioral risks associated with irregular investing.

Abhishek increased his monthly retirement allocation through VPF contributions instead of relying entirely on discretionary investments.

The PF calculator allowed him to model multiple scenarios.

| Monthly Additional Contribution | Estimated Long-Term Impact |

|---|---|

| ₹5,000 | Significant increase in retirement corpus |

| ₹10,000 | Accelerated long-term compounding |

| ₹15,000 | Higher retirement income stability |

The simulations demonstrated how relatively small increases during the earning years could create disproportionately large outcomes over 20 to 25 years.

This visualization helped convert abstract financial advice into measurable action.

2. Separating Retirement From Family Goals

Another major insight involved goal separation.

Before using the calculator, Abhishek had mentally grouped multiple future obligations into one broad category called “savings.” In practice, however, retirement planning competes with several other long-term financial objectives.

These included:

- Daughter’s higher education

- Marriage expenses

- Home loan obligations

- Emergency reserves

- Retirement income

The calculator made it evident that using retirement assets for family milestones would weaken post-retirement financial security.

As a result, he created separate investment buckets.

Retirement remained centered around EPF, VPF, and long-term accumulation tools. Meanwhile, future education and marriage expenses were shifted toward equity-oriented mutual funds with longer growth potential.

Projected education and marriage costs were estimated at approximately ₹95 lakh under inflation-adjusted assumptions.

This restructuring introduced clarity into his financial planning process. Instead of treating all investments interchangeably, each allocation now served a distinct future purpose.

3. Rebalancing Toward Equity Exposure

The third strategic shift involved portfolio diversification.

Prior to the exercise, a significant portion of Abhishek’s long-term savings was concentrated in relatively conservative instruments including EPF, fixed deposits, and traditional insurance products.

The PF calculator highlighted that while debt-oriented instruments provide stability, they may not independently generate sufficient real returns over long periods.

He began viewing EPF as the “debt allocation” within his retirement framework rather than the entire retirement strategy itself.

This led to a gradual increase in equity exposure through:

- Equity mutual funds

- Index-based SIPs

- Long-term diversified funds

The objective was not short-term wealth creation. Instead, it was to improve the probability of achieving an inflation-adjusted retirement target estimated at approximately ₹9.3 crore.

Importantly, the transition was phased and disciplined. The emphasis remained on asset allocation balance rather than aggressive speculation.

The Psychological Role of Financial Calculators

One of the most overlooked functions of PF calculators is behavioral impact.

Financial planning advice often fails because future risks feel abstract. Numbers written in reports rarely create emotional urgency unless individuals can directly connect them to their own lives.

In Abhishek’s case, the calculator transformed passive awareness into active planning.

Three specific behavioral effects stood out.

Inflation Awareness

The calculator replaced the illusion of future wealth with inflation-adjusted reality.

Without inflation modeling, retirement projections can appear deceptively comfortable. Once purchasing power adjustments were introduced, the shortfall became immediately visible.

This altered savings behavior more effectively than generic financial advice.

Visibility of Compounding

The salary growth projections demonstrated how future raises could materially increase long-term wealth if contribution rates also increased over time.

Instead of treating salary hikes as lifestyle upgrades alone, Abhishek began allocating portions of future increments toward long-term investments.

Action-Oriented Planning

The calculator converted vague concerns into measurable gaps.

Rather than asking:

“Am I saving enough?”

The planning process evolved into:

“How much more is required to reach the target?”

This change simplified decision-making.

Broader Lessons for Salaried Employees

This case reflects a broader issue within salaried financial planning across India.

Many employees assume EPF alone guarantees retirement security because the system is structured, mandatory, and government-backed. While EPF remains one of the most tax-efficient long-term instruments available under the EEE framework, retirement adequacy depends on multiple variables beyond contribution consistency.

These include:

- Inflation

- Career growth

- Longevity

- Healthcare inflation

- Family obligations

- Asset allocation

- Tax planning

- Lifestyle expectations

PF calculators help bridge the gap between passive saving and active retirement planning by quantifying future realities.

For mid-career professionals, especially those between 30 and 45 years old, the timing of this realization can materially alter long-term outcomes. Early adjustments require smaller corrective actions. Delayed adjustments often require disproportionately larger savings rates later in life.

Final Outcome

By 2025, roughly three years after the initial calculation exercise, Abhishek had significantly restructured his financial approach.

Key changes included:

- Higher retirement contribution rates through VPF

- Dedicated equity allocations for long-term family goals

- Improved diversification across debt and equity assets

- Inflation-adjusted retirement planning targets

- More disciplined annual review processes

Most importantly, the planning process became proactive rather than reactive.

The PF calculator did not generate wealth by itself. What it provided was visibility.

That visibility created urgency, and urgency created action.

The Real Value of a PF Calculator

Retirement planning failures rarely occur because individuals refuse to save. More often, they happen because future requirements are underestimated for too long.

For salaried employees, PF accounts create a valuable financial foundation, but they can also create false comfort when viewed in isolation. Financial Calculators and projection tools help convert assumptions into measurable outcomes by exposing the gap between current savings trajectories and future financial realities.

In Abhishek Patel’s case, the most important outcome was not the projected corpus figure itself. It was the realization that there was still enough time to correct the gap.

That realization fundamentally changed how he approached money, risk, retirement, and long-term financial security.