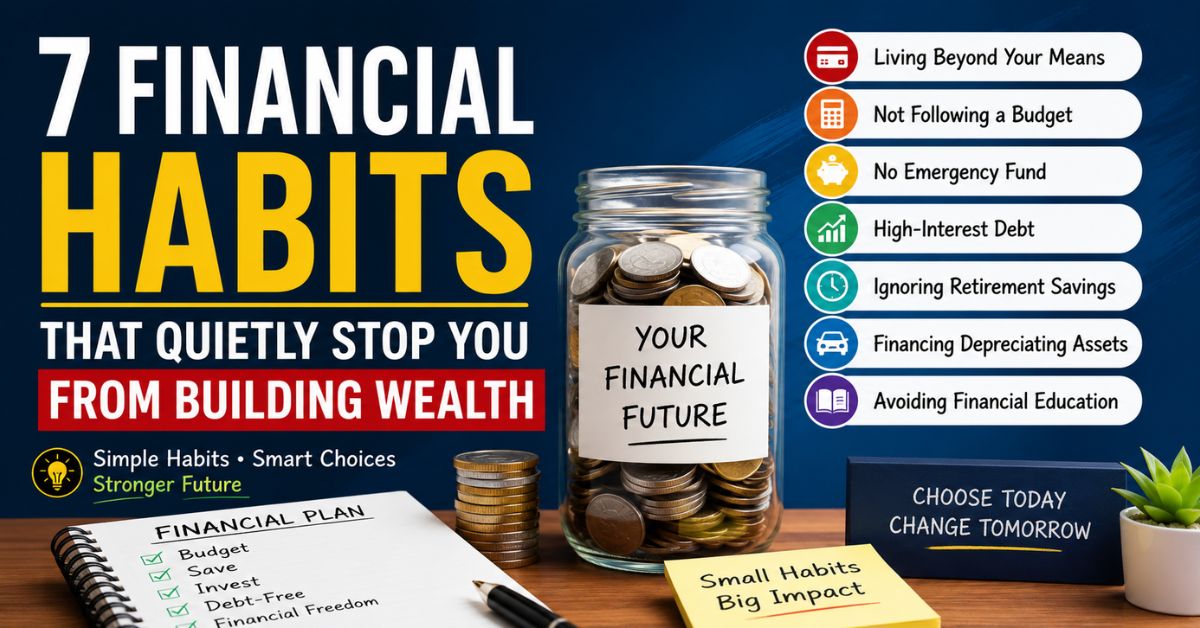

7 Financial Habits That Quietly Keep People Stuck: Key Highlights

- Living beyond your means can create a debt cycle that slows wealth building.

- A budget helps you understand where your money is going and improves financial control.

- An emergency fund provides protection against unexpected expenses and financial setbacks.

- High-interest debt can consume a large portion of income and delay financial progress.

- Starting retirement and long-term savings early allows compound growth to work in your favor.

- Financing depreciating assets can reduce your ability to save and invest for the future.

- Financial education and planning tools can help you make better money decisions over time.

Money problems rarely appear overnight. In most cases, they develop slowly through small financial decisions that seem harmless at the time. A daily coffee, an extra subscription, a few impulse purchases, or a delayed savings plan may not feel significant individually. However, when these habits continue for months or years, they can have a major impact on your financial future.

Many people assume that earning more money automatically leads to financial success. While income certainly matters, your financial habits often play an even bigger role. There are people with high salaries who struggle financially, and there are people with average incomes who steadily build wealth. The difference often comes down to how they manage their money.

The good news is that bad financial habits can be changed. Once you identify the behaviors that are holding you back, you can take practical steps to improve your financial health and move closer to your long-term goals.

Here are seven common financial habits that quietly prevent people from building wealth and what you can do to avoid them.

💡 Helpful Tool For Readers: Plan Your Financial Future Better

📊 Explore Financial Planning Calculators1. Living Beyond Your Means

One of the biggest financial mistakes people make is spending more than they earn.

This habit often starts innocently. A larger apartment, a newer car, frequent dining out, luxury purchases, or expensive vacations may seem manageable at first. The problem arises when these expenses consistently exceed your income.

Many people rely on credit cards, personal loans, or buy-now-pay-later services to maintain a lifestyle they cannot comfortably afford. Over time, debt begins to accumulate, and interest payments consume an increasing portion of monthly income.

This creates a cycle where a significant amount of money goes toward paying for past purchases rather than building future wealth.

How to Fix It

Start by reviewing your monthly income and expenses.

Ask yourself:

- Are you spending more than you earn?

- Are you relying on debt to cover routine expenses?

- Are there lifestyle costs that can be reduced?

A simple rule is to ensure your expenses remain below your income. The gap between what you earn and what you spend becomes your opportunity to save and invest.

Building wealth becomes much easier when you consistently live below your means.

2. Not Following a Budget

Many people avoid budgeting because they think it is restrictive or complicated.

In reality, a budget simply tells your money where to go before it disappears.

Without a budget, it is easy to underestimate spending. Small expenses often go unnoticed because they do not seem significant in the moment. Food delivery, online shopping, streaming subscriptions, app purchases, and daily convenience spending can quietly drain hundreds or even thousands of dollars each year.

A budget creates awareness. It helps you understand your spending patterns and identify areas where money may be leaking.

How to Fix It

Start by tracking every expense for one month.

You do not need advanced software. A spreadsheet, notebook, or budgeting app can work just as well.

Many financial experts recommend the 50/30/20 rule:

- 50% for needs such as housing, food, utilities, and transportation

- 30% for wants such as entertainment and dining out

- 20% for savings and debt repayment

This framework provides a simple starting point that can be adjusted based on your financial situation.

The goal is not perfection. The goal is awareness and control.

3. Neglecting an Emergency Fund

Unexpected expenses are a normal part of life.

Medical bills, home repairs, vehicle maintenance, family emergencies, and job losses can happen without warning.

Unfortunately, many people are financially unprepared when these situations arise. Without an emergency fund, they often turn to credit cards or loans, which can create long-term debt problems.

An emergency fund acts as a financial safety net. It helps you handle unexpected events without disrupting your financial progress.

How to Fix It

Aim to save enough money to cover three to six months of essential living expenses.

If that amount feels overwhelming, start small.

Your first goal could be:

- $500

- $1,000

- One month of expenses

Consistency matters more than the starting amount.

Even small contributions made regularly can build a strong emergency fund over time.

Treat emergency savings as a necessity rather than an optional financial goal.

4. Carrying High-Interest Debt

High-interest debt is one of the biggest obstacles to financial growth.

Credit card debt is especially dangerous because interest rates can be extremely high. When you only make minimum payments, a large portion of your payment goes toward interest rather than reducing the original balance.

This means you may spend years paying for purchases that you no longer use or even remember.

The longer debt remains unpaid, the more expensive it becomes.

How to Fix It

Create a debt repayment plan.

Two popular approaches include:

Debt Snowball Method

Pay off the smallest debt first while making minimum payments on the others.

This method creates quick wins and can help maintain motivation.

Debt Avalanche Method

Focus on the debt with the highest interest rate first.

This approach often saves more money over time.

Whichever strategy you choose, prioritize eliminating high-interest debt before pursuing aggressive investment goals.

Reducing expensive debt is often one of the best financial decisions you can make.

5. Ignoring Retirement and Long-Term Savings

Many people delay saving for retirement because it feels far away.

A person in their twenties or thirties may believe they have plenty of time to start later. Unfortunately, delaying savings can significantly reduce future wealth because it limits the power of compound growth.

Compound growth occurs when your earnings begin generating additional earnings over time. The earlier you start, the longer your money has to grow.

Even modest monthly contributions can become substantial over several decades.

How to Fix It

Start investing as early as possible.

The amount is less important than consistency.

- Contributing a small amount every month for 30 years can often produce better results than contributing a larger amount for only 10 years.

- Regular investing allows you to benefit from long-term market growth and compounding.

If your employer offers retirement benefits or matching contributions, take advantage of them whenever possible.

The key is to start now rather than waiting for the perfect moment.

6. Financing Depreciating Assets

Some purchases lose value quickly after they are bought.

Cars, smartphones, consumer electronics, and many luxury goods typically become less valuable over time.

While there is nothing wrong with purchasing these items when needed, financing them through loans or lengthy installment plans can create unnecessary financial pressure.

In many cases, people end up paying interest on an asset that is steadily losing value.

This combination can slow wealth building considerably.

How to Fix It

Before making a major purchase, ask yourself:

- Do I truly need this item?

- Can I save and pay cash instead?

- Is there a quality pre-owned option available?

- Will this purchase improve my financial future or delay it?

Choosing practical alternatives can free up money for savings, investments, and long-term financial goals.

The objective is not to avoid spending entirely. It is to spend intentionally.

7. Avoiding Financial Education

Many people find financial topics intimidating.

Terms such as inflation, asset allocation, diversification, interest rates, tax planning, and investing can seem complicated at first. As a result, some individuals avoid learning about money altogether.

Unfortunately, financial ignorance can be expensive.

Without basic financial knowledge, people are more likely to:

- Fall for poor investment advice

- Accumulate unnecessary debt

- Miss tax-saving opportunities

- Make emotional financial decisions

- Delay important financial planning

Financial education does not require a finance degree. A basic understanding of money management can dramatically improve financial outcomes.

How to Fix It

Dedicate time each month to learning about personal finance.

- Read financial blogs

- Follow reputable financial educators

- Listen to finance podcasts

- Watch educational videos

- Use financial planning tools

Even 15 to 20 minutes of learning each week can help you make smarter financial decisions over time.

Knowledge often becomes one of the highest-return investments you can make.

How Financial Calculators Can Help You Make Better Money Decisions

One of the easiest ways to improve your financial planning is by using financial calculators.

Many people struggle with budgeting because they estimate rather than calculate. This often leads to unrealistic savings goals, inaccurate investment expectations, and poor debt management decisions.

Financial calculators remove the guesswork.

They help you understand:

- How much you should save each month

- How long it may take to reach a financial goal

- How much wealth can grow through regular investing

- How loan repayments affect your finances

- Whether your budget aligns with your income and goals

For example, if you want to build an emergency fund, a calculator can help determine how much you need to save each month to reach your target within a specific timeframe.

Similarly, retirement and investment calculators can show the long-term impact of consistent contributions and compound growth.

If you are looking for tools to improve budgeting, savings planning, investment calculations, and overall financial management, you can explore the Financial Planning Calculators.

Using calculators regularly can help transform financial planning from guesswork into a data-driven process.

Simple Habits That Can Help You Break the Cycle

Improving your finances does not require dramatic changes.

Small, consistent actions often produce the best results.

Audit Your Subscriptions

Review your bank and credit card statements.

Cancel subscriptions that you no longer use or need.

Many people are surprised by how much they spend on forgotten recurring charges.

Automate Your Savings

Set up automatic transfers to your savings account on payday.

This approach removes the temptation to spend money before saving it.

Follow the 24-Hour Rule

Before making a non-essential purchase, wait 24 hours.

In many cases, the urge to buy fades, helping you avoid impulse spending.

Set Clear Financial Goals

People are more likely to save when they have a purpose.

- Building an emergency fund

- Buying a home

- Starting a business

- Funding education

- Preparing for retirement

Specific goals provide motivation and direction.

Review Your Finances Monthly

Spend 30 minutes each month reviewing:

- Income

- Expenses

- Savings progress

- Debt balances

- Financial goals

Regular reviews help you stay on track and identify problems before they become serious.

Final Thoughts

Financial success is rarely determined by a single decision. More often, it is the result of hundreds of small choices made consistently over time.

Living beyond your means, ignoring a budget, carrying high-interest debt, neglecting emergency savings, delaying retirement contributions, financing depreciating assets, and avoiding financial education can quietly hold you back for years.

The encouraging news is that every one of these habits can be changed.

You do not need a massive income increase, a winning investment, or a perfect financial plan to improve your situation. What you need is awareness, consistency, and a willingness to make better financial decisions one step at a time.

By building healthy money habits, using financial planning tools, and staying committed to long-term goals, you can create a stronger financial future and move closer to lasting financial freedom.