Article Highlights

- PF withdrawal amount depends on your employee share, employer contribution, and total service period.

- EPFO’s digital upgrade has made many Aadhaar-linked claims faster through auto-settlement.

- Tax deduction may apply if you withdraw PF before completing five years of continuous service.

- Different withdrawal reasons such as unemployment, medical emergencies, or home purchase have separate limits.

- Users can estimate their PF payout by checking their EPF passbook and applying the latest withdrawal rules.

For many salaried employees in India, the Employees’ Provident Fund, or EPF, is one of the largest long-term savings accounts connected to their job. Over the years, monthly contributions from both employees and employers slowly build into a retirement corpus that can also help during emergencies, unemployment, medical expenses, or home purchases.

However, many PF subscribers still struggle to understand one basic question before filing a claim: how much money can actually be withdrawn?

The answer is not always simple because PF withdrawal calculations depend on multiple factors including your total balance, years of service, reason for withdrawal, tax rules, and eligibility conditions set by the Employees’ Provident Fund Organisation (EPFO).

In 2026, the process has become easier due to the digital reforms commonly referred to as “EPFO 3.0.” Aadhaar-based verification, automatic claim settlement, and online processing have reduced paperwork for many users. But estimating the final amount that reaches your bank account still requires understanding a few important rules.

Here is a complete guide explaining how PF withdrawal amount is estimated in 2026.

What Makes Up Your Total PF Balance

Before calculating your withdrawal amount, users must first understand what their EPF balance includes.

Your total PF balance is generally made up of three components:

- Employee contribution

- Employer contribution to EPF

- Interest earned on both contributions

Every month, 12 percent of your basic salary and dearness allowance is contributed towards EPF from your salary. Your employer also contributes 12 percent, although a part of this amount goes into the Employee Pension Scheme, or EPS.

The EPFO adds annual interest to the EPF balance. For FY 2025-26, the EPF interest rate remains 8.25 percent.

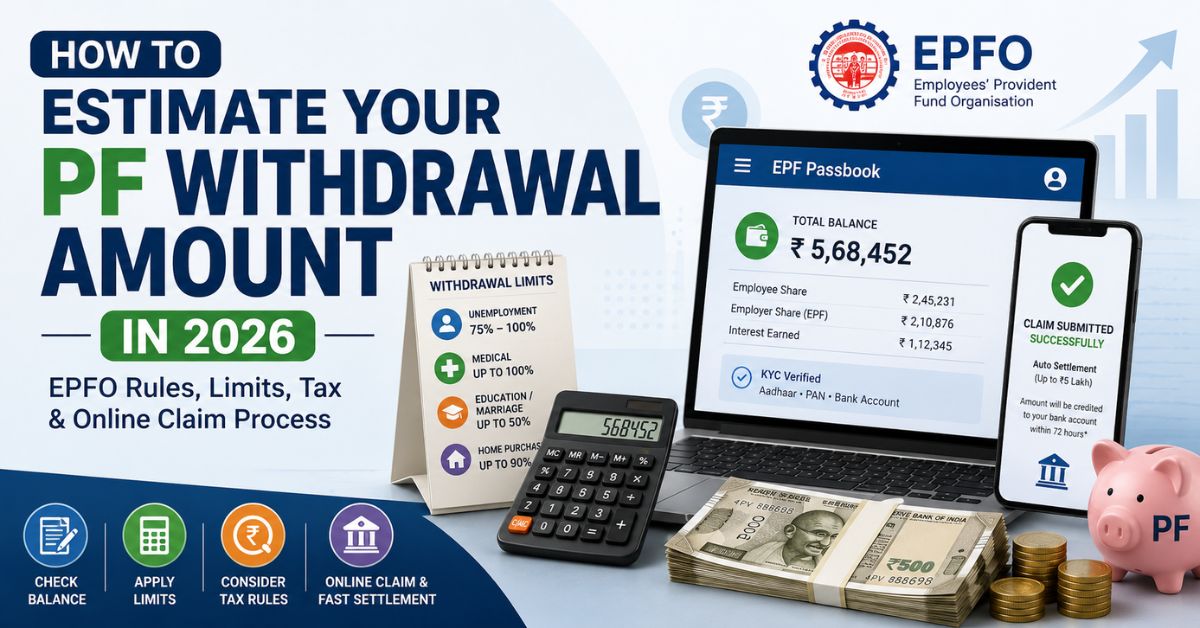

Users can check all these figures through the EPF passbook available on the UAN Member Portal.

How to Check Your PF Passbook

The EPF passbook is the most important document for estimating your withdrawal amount.

It shows:

- Employee share

- Employer share

- Monthly deposits

- Interest credited

- Total accumulated balance

To access it, users need an activated Universal Account Number (UAN).

The process includes:

- Visit the EPFO Member Passbook portal

- Log in using UAN and password

- Select the PF account linked to your employer

- Download or view the passbook

The balance shown here forms the base for withdrawal calculations.

Why Your Withdrawal Reason Matters

The amount you can withdraw depends heavily on why you are applying for PF withdrawal.

EPFO allows both partial withdrawals and full settlements. Different conditions apply to each category.

In 2026, these are some of the commonly used withdrawal categories.

PF Withdrawal During Unemployment

Employees who lose their jobs or remain unemployed can withdraw a large part of their PF balance.

The current rules are:

| Unemployment Period | Withdrawal Limit | Condition |

|---|---|---|

| After 1 month | Up to 75% of total balance | 25% balance remains in account |

| After 2 months | Up to 100% of total balance | Full settlement allowed |

For example, if your total PF balance is ₹4 lakh and you remain unemployed for one month, you may be eligible to withdraw up to ₹3 lakh.

After two months, the full amount can generally be withdrawn.

PF Withdrawal for Medical Emergencies

EPFO also allows partial withdrawal during medical emergencies.

The maximum amount is usually the lower of:

- Six months’ basic salary plus DA

- Total employee contribution with interest

Medical withdrawals do not usually require a minimum service period.

Under the digital auto-settlement system introduced by EPFO, eligible advance claims up to ₹5 lakh can now be processed faster for many users.