PF Contribution Rules Explained

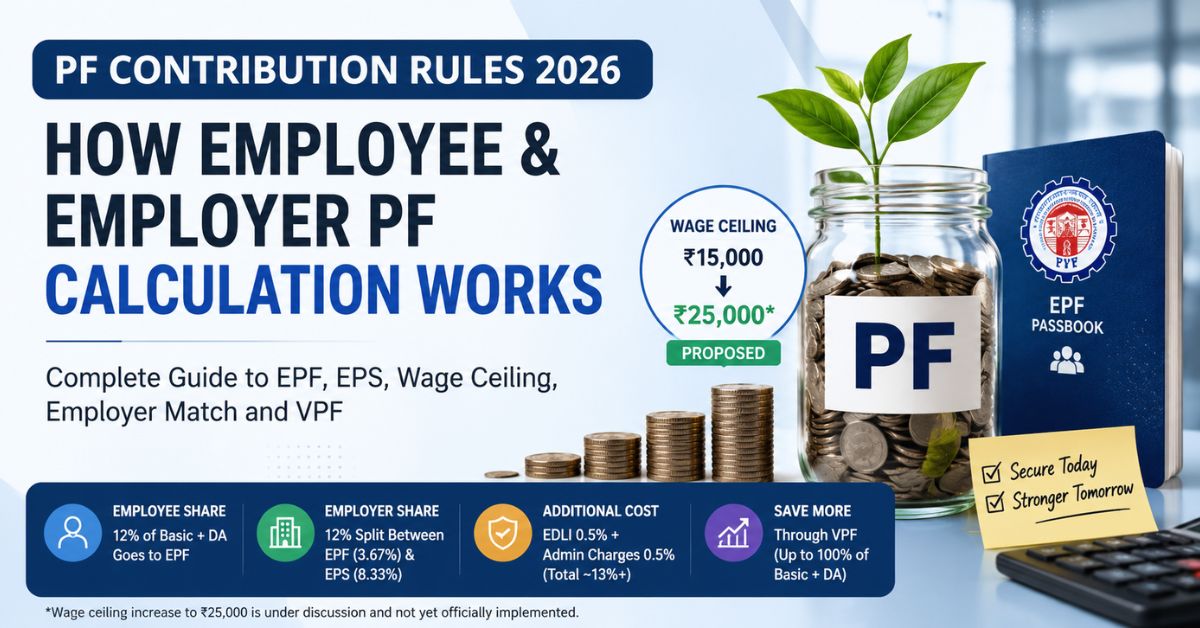

- Both employees and employers contribute 12% of Basic Salary and Dearness Allowance towards PF.

- The employer contribution is split between EPF and EPS, which often confuses salaried employees.

- The current statutory wage ceiling remains ₹15,000, though discussions around a ₹25,000 limit continue.

- Many employers cap their PF contribution at the statutory ceiling even when employee salaries are much higher.

- Employees can increase retirement savings through VPF, but extra employer matching is not mandatory.

For salaried employees in India, Provident Fund deductions are one of the most common parts of the monthly salary slip. Yet many employees still do not fully understand how PF contributions are calculated, how much employers actually contribute, or why the final amount credited to the account is often lower than expected.

The confusion usually begins with the idea of “matching contribution.” Most employees assume that if they contribute 12% of their salary, the employer also deposits the same amount directly into the PF account. In reality, the employer contribution is divided into multiple components including the Employee Pension Scheme, or EPS.

In 2026, PF contribution calculations are drawing even more attention because of discussions around increasing the statutory wage ceiling from ₹15,000 to ₹25,000. If implemented in future reforms, the change could significantly increase employer contributions for many salaried workers.

Here is a detailed explanation of how PF contribution calculations work, how employer matching actually functions, and what the proposed wage ceiling revision could mean for employees.

What is the PF Contribution Structure?

The Employees’ Provident Fund system is managed by the Employees’ Provident Fund Organisation, or EPFO.

Under standard EPF rules, both the employee and employer contribute 12% of the employee’s Basic Salary plus Dearness Allowance every month.

The contribution does not apply to the full salary package shown in the CTC. Components like House Rent Allowance, special allowance, bonus, incentives, and travel allowance are generally excluded from PF calculations unless specifically structured otherwise by the employer.

This means the PF deduction depends mainly on Basic Salary and Dearness Allowance.

How Employee PF Contribution Works

The employee contribution process is straightforward.

- 12% of Basic Salary + DA is deducted from salary every month

- The full amount goes directly into the EPF account

- The balance earns annual EPF interest

For example, if an employee’s Basic Salary is ₹50,000:

| Calculation | Amount |

|---|---|

| Basic Salary | ₹50,000 |

| Employee PF Contribution (12%) | ₹6,000 |

This entire ₹6,000 goes into the EPF account.

How Employer PF Contribution Actually Works

The employer contribution is where most confusion begins.

Although employers also contribute 12%, the entire amount does not go into the EPF account.

Instead, the contribution is split into two major parts:

| Component | Employer Share | Purpose |

|---|---|---|

| EPF | 3.67% | Added to PF balance and earns EPF interest |

| EPS | 8.33% | Used for pension eligibility under EPS |

This means only a smaller part of the employer contribution directly increases the PF balance.

The remaining amount goes into the pension scheme.

Understanding the Employee Pension Scheme (EPS)

The Employee Pension Scheme is linked to long-term retirement pension benefits.

Unlike EPF:

- EPS does not earn annual EPF interest

- The amount is not visible as a normal growing PF balance

- EPS helps employees build pension eligibility after retirement

This is why employees often notice that the employer contribution shown in salary slips does not fully appear inside the PF passbook balance.

The Additional Employer Cost Beyond 12%

Apart from the standard 12% contribution, employers also pay additional statutory charges.

These include:

| Additional Component | Rate |

|---|---|

| EDLI Insurance | 0.5% |

| EPF Admin Charges | 0.5% |

This takes the employer’s total statutory PF-related cost to slightly above 13% of Basic Salary in most cases.

The EDLI component acts as a life insurance benefit linked to EPF membership.

The Most Important PF Concept: Wage Ceiling

One of the biggest reasons for PF confusion is the wage ceiling rule.

Under current EPFO rules, the statutory wage ceiling for EPS contribution is ₹15,000.

This ceiling affects how much employers are required to contribute.

What Happens If Salary is Below ₹15,000?

If an employee earns below the ceiling:

- Employee contributes 12% on actual salary

- Employer also contributes 12% on actual salary

For example:

| Salary Component | Amount |

|---|---|

| Basic Salary | ₹12,000 |

| Employee Contribution | ₹1,440 |

| Employer Contribution | ₹1,440 |

In this situation, both contributions are calculated on the full salary.

What Happens If Salary is Above ₹15,000?

This is where the “PF ceiling trap” becomes important.

Suppose an employee earns:

- Basic Salary = ₹75,000

In many companies:

- Employee contribution is calculated on the full salary

- Employer contribution remains capped at the statutory ceiling

That means:

| Salary Component | Amount |

|---|---|

| Basic Salary | ₹75,000 |

| Employee EPF Contribution | ₹9,000 |

| Employer EPS Contribution | ₹1,250 |

| Employer EPF Contribution | ₹550 |

| Total Employer Contribution | ₹1,800 |

This surprises many employees because they contribute ₹9,000 while the employer contributes only ₹1,800.

However, this structure is allowed because of the statutory ceiling.

Why PF Contributions Differ Between Companies

Not all employers follow identical PF structures.

Some employers contribute PF on:

- Full Basic Salary

- Restricted statutory ceiling

- Fixed salary structures

This is why two employees earning the same salary may still receive different PF contributions depending on company policy.

Employees should always check salary structure, offer letter, CTC breakup, and PF deduction details before assuming employer matching works equally.

Proposed Wage Ceiling Increase to ₹25,000

Policy discussions around EPFO reforms include a proposal to increase the statutory wage ceiling from ₹15,000 to ₹25,000.

The proposal has not yet been fully implemented officially, but it is being discussed as part of broader labour and social security reforms.

If implemented, the change could increase employer contributions significantly.

How the Proposed Ceiling Could Change PF Contributions

Under the current ₹15,000 ceiling:

| Component | Current Ceiling (₹15,000) |

|---|---|

| Employer EPS Contribution | ₹1,250 |

| Employer EPF Contribution | ₹550 |

| Total Employer Contribution | ₹1,800 |

If the ceiling rises to ₹25,000:

| Component | Proposed Ceiling (₹25,000) |

|---|---|

| Employer EPS Contribution | ₹2,083 |

| Employer EPF Contribution | ₹917 |

| Total Employer Contribution | ₹3,000 |

This would increase retirement savings for many employees over the long term.

Voluntary Provident Fund (VPF) Explained

Employees who want to save more can choose Voluntary Provident Fund or VPF.

- Employees can contribute beyond the mandatory 12%

- Contributions can go up to 100% of Basic Salary + DA

- The amount earns the same EPF interest rate

However, the employer is not required to match VPF contributions.

This means the additional saving comes entirely from the employee side.

Tax Rules on Higher PF Contributions

PF remains one of the most tax-efficient savings tools under the Exempt-Exempt-Exempt structure.

However, taxation rules changed for higher contributions.

If total employee contributions to EPF and VPF exceed ₹2.5 lakh in a financial year, the interest earned on the excess contribution becomes taxable.

This rule mainly affects high-income salaried employees, senior professionals, and employees making large VPF contributions.

Why Understanding PF Calculations Matters

Many salaried employees focus only on monthly salary credits without fully understanding retirement savings structures.

But PF contributions directly affect long-term wealth creation, retirement savings, pension eligibility, tax planning, and salary negotiations.

Even small monthly contribution differences can create a major impact after 20 to 30 years because of compounding.

As EPFO reforms continue and wage ceiling discussions move forward, understanding how PF calculations actually work is becoming increasingly important for salaried employees across India.