PF vs PPF: Key Points Investors Should Know

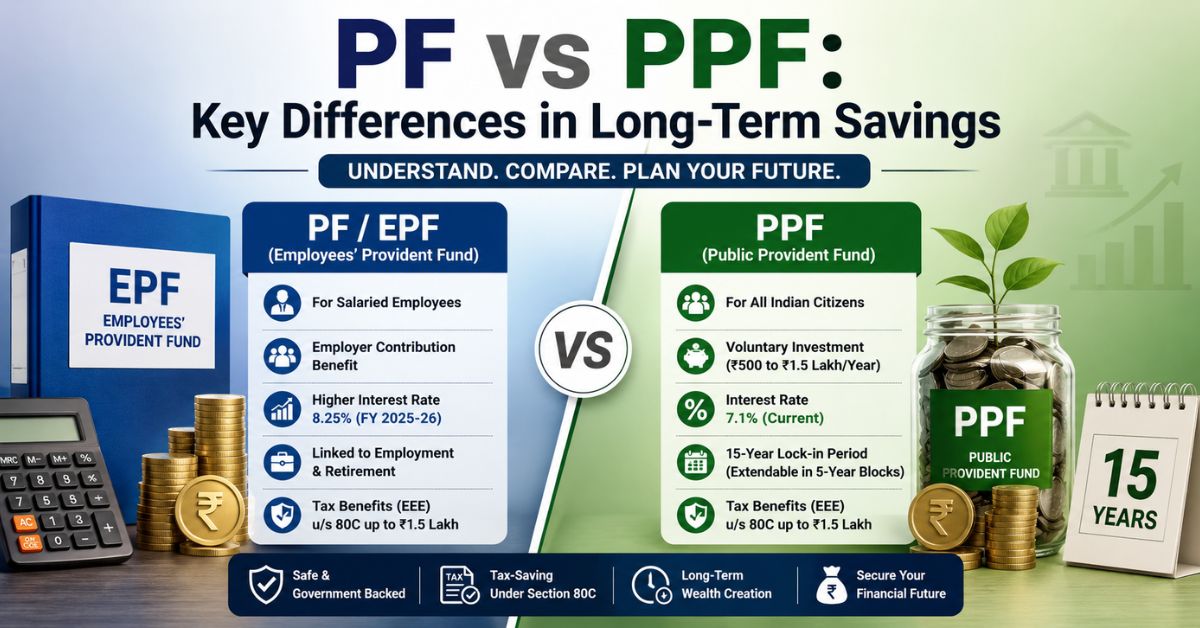

- EPF is designed for salaried employees, while PPF is open to all Indian citizens including freelancers and self-employed individuals.

- EPF currently offers 8.25% interest for FY 2025-26, while PPF offers 7.1% interest.

- EPF includes employer contribution benefits, whereas PPF is entirely voluntary without employer matching.

- Both schemes qualify for tax deductions under Section 80C and offer tax-free maturity benefits.

- Financial planners often recommend using EPF as a retirement base and PPF as an additional long-term savings instrument.

For many Indians, Provident Fund investments are among the safest ways to build long-term savings. However, confusion between PF and PPF remains common because both names sound similar and both offer tax-free returns. In reality, the two schemes are designed for different types of investors and serve different financial purposes.

PF, commonly called EPF or Employees’ Provident Fund, is mainly meant for salaried employees working in organised sectors. PPF, or Public Provident Fund, is a government-backed savings scheme available to all Indian citizens, including freelancers and self-employed individuals.

While both schemes help create long-term wealth, their contribution structure, withdrawal rules, lock-in period, and flexibility are very different. Understanding these differences becomes important for investors planning retirement, tax savings, or future financial goals.

Why PF and PPF Matter for Long-Term Savings

Long-term savings products are becoming increasingly important as inflation continues to affect household expenses and retirement planning. Fixed deposits often struggle to beat inflation after taxes, while market-linked investments can carry higher risks for conservative investors.

This is where PF and PPF continue to remain popular. Both schemes offer stable returns, government-backed security, and tax benefits under Section 80C of the Income Tax Act.

For salaried employees, PF acts as a compulsory retirement savings mechanism. For self-employed individuals, PPF provides a disciplined way to create a long-term corpus with sovereign protection.

What is PF or EPF?

The Employees’ Provident Fund Organisation (EPFO) manages the Employees’ Provident Fund scheme for salaried workers in India.

Under EPF rules, employees contribute 12% of their basic salary and dearness allowance every month. Employers also contribute an equivalent amount, although part of the employer contribution goes into the Employees’ Pension Scheme (EPS).

The biggest advantage of EPF is the employer contribution. This additional contribution helps employees build retirement savings much faster than most traditional savings products.

For FY 2025-26, the EPF interest rate remains at 8.25%, making it one of the higher-yielding fixed-income retirement products available to salaried investors.

EPF accounts also receive yearly compounded interest, which helps the corpus grow steadily over long periods.

What is PPF?

The Public Provident Fund (PPF) scheme is administered through banks and post offices under the Government’s small savings framework.

Unlike EPF, PPF is completely voluntary. Any Indian citizen can open a PPF account, including freelancers, small business owners, students, and non-salaried individuals.

Investors can deposit between ₹500 and ₹1.5 lakh annually into a PPF account. The current interest rate stands at 7.1%.

PPF comes with a 15-year lock-in period, although investors can extend the account further in blocks of five years after maturity.

The scheme remains popular because of its government guarantee and tax-free maturity benefits.

PF vs PPF: Major Differences Explained

Although both schemes fall under provident fund investments, they work very differently in practice.

| Feature | EPF | PPF |

|---|---|---|

| Eligibility | Salaried employees | All Indian citizens |

| Contribution Type | Mandatory salary deduction | Voluntary investment |

| Employer Contribution | Yes | No |

| Interest Rate | 8.25% | 7.1% |

| Lock-in Period | Linked to employment | 15 years |

| Tax Benefits | EEE | EEE |

Contribution Structure and Employer Benefits

EPF follows a compulsory contribution system linked to salary. Employees contribute 12% of their basic salary and dearness allowance every month.

Employers also contribute an additional 12%, although a portion goes into the Employees’ Pension Scheme instead of the EPF account.

PPF works differently. Investors can decide how much to contribute every year within the allowed limits. There is no employer contribution or mandatory deduction.

Interest Rates and Long-Term Compounding

EPF generally offers higher returns than PPF. The EPF interest rate currently stands at 8.25%, while PPF offers 7.1%.

EPF returns are linked to earnings generated by the EPFO through debt investments and limited exposure to equity-linked exchange traded funds.

PPF interest rates are decided quarterly by the Government and are generally considered more stable.

Over long investment periods, even small differences in interest rates can create a significant gap in the final retirement corpus because of compounding.

Withdrawal Rules and Liquidity

PPF has a strict 15-year lock-in period. Partial withdrawals are allowed from the seventh financial year after the account is opened.

Loans against PPF are allowed between the third and sixth financial years.

EPF offers comparatively greater flexibility for withdrawals under specific conditions such as medical emergencies, home purchase, higher education, marriage expenses, unemployment, or retirement.

Online withdrawal systems introduced by the EPFO have also improved the claim settlement process in recent years.

Tax Benefits Under Section 80C

Both EPF and PPF qualify for tax deductions under Section 80C up to the overall annual limit of ₹1.5 lakh.

Both investments also enjoy EEE status, meaning contributions, interest earned, and maturity proceeds remain tax-free under existing rules.

However, EPF has an additional tax condition for higher-income earners. Interest earned on employee EPF contributions above ₹2.5 lakh annually becomes taxable when the employer also contributes to the EPF account.

Which Investment is Better?

For salaried employees, financial planners usually recommend prioritising EPF contributions because of the employer contribution advantage.

The additional contribution from employers helps increase long-term retirement savings without requiring extra investment from the employee.

PPF is often considered more suitable for freelancers, self-employed professionals, and conservative investors looking for stable long-term savings with government backing.

Many families also use PPF accounts for long-term goals such as children’s higher education or retirement planning.

Can Investors Use Both Together?

Many investors use both EPF and PPF together as part of their financial planning strategy.

EPF can serve as the primary retirement savings product for salaried employees, while PPF can act as an additional tax-free savings instrument.

However, investors should remember that both schemes fall under the same ₹1.5 lakh Section 80C deduction limit.

For example, if an employee’s annual EPF contribution already reaches ₹1.2 lakh, only ₹30,000 of additional Section 80C deduction space remains available for PPF investments.

Risk and Safety Comparison

Both EPF and PPF are considered low-risk investment products compared to market-linked assets.

PPF carries sovereign backing from the Government of India, making it one of the safest long-term savings options available.

EPF is also highly secure because it operates under government supervision through the EPFO.

However, EPF has limited exposure to equity-linked investments through ETFs, which partly explains why EPF returns are usually slightly higher than PPF returns.

Long-Term Savings Choices for Young Investors

For young salaried professionals, EPF often becomes the foundation of retirement planning because of automatic salary deductions and employer contributions.

For self-employed individuals without access to EPF, PPF remains one of the strongest government-backed long-term savings schemes available in India.

Financial advisers also suggest that investors should avoid depending entirely on only one product for retirement planning. Along with provident fund investments, long-term portfolios may also require equity mutual funds or other growth-oriented investments to manage inflation over time.

Even so, PF and PPF continue to remain important pillars of long-term financial planning because of their safety, tax efficiency, and disciplined savings structure.