The Rise of the Unbreakable SIP Investor: How Retail Investors Are Redefining Wealth Creation During Market Volatility

Platform: Vittarthi Financial Research

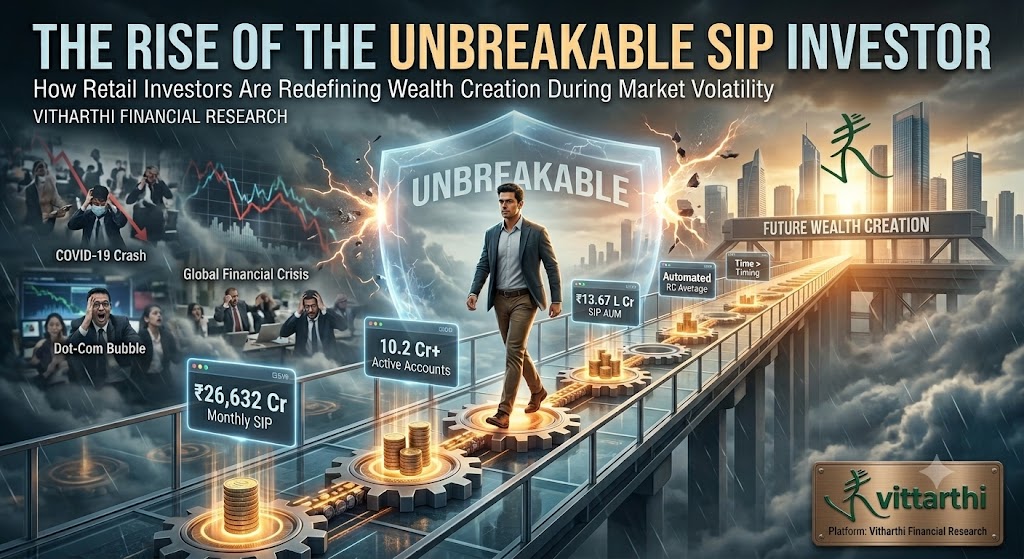

₹26,632 Cr

Monthly SIP Inflow (Dec 2024)

10.2 Cr+

Active SIP Accounts in India

₹13.67 L Cr

Total AUM via SIPs (2024)

Executive Summary

The investment landscape has undergone a dramatic transformation over the last decade. Historically, retail investors reacted emotionally to market volatility — selling during downturns and returning only after markets had recovered. This behavior frequently resulted in poor long-term returns and missed opportunities.

Despite inflation concerns, geopolitical tensions, interest rate uncertainty, and market corrections, investors continue contributing to Systematic Investment Plans (SIPs) at record levels. This phenomenon — referred to in this Vittarthi case study as the "Unbreakable SIP Investor" — represents a significant behavioral shift in personal finance. Rather than viewing market declines as threats, investors increasingly perceive them as opportunities to accumulate assets at lower prices.

The purpose of this case study is to examine:

- Why investor behavior is changing.

- How SIP investing has become a preferred wealth creation strategy.

- The role of financial literacy and technology.

- Why Flexi-Cap Funds have gained popularity.

- What lessons investors can learn from this transformation.

Introduction: The Historical Cycle of Fear and Greed

Financial markets have always been driven by two powerful emotions: Fear and Greed. When markets rise rapidly, greed encourages investors to chase returns. When markets fall sharply, fear drives them to exit. For decades, these emotional cycles defined retail investor behavior worldwide.

⚠ The Traditional Investment Trap

- Markets rise and investors become optimistic.

- More money enters the market.

- A correction occurs, and panic spreads.

- Investors withdraw money at the worst possible time.

- Markets recover, but investors return too late — missing the rebound.

This cycle repeated through multiple economic events: the Dot-Com Bubble (2000), the Global Financial Crisis (2008–09), the European Debt Crisis (2011), and the COVID-19 Market Crash (2020). Yet something unusual is happening today.

📊 A Behavioral Turning Point

During the COVID-19 market crash of March 2020, the Nifty 50 fell ~38% in just 40 days. Despite this, AMFI data shows that SIP inflows did not collapse — monthly contributions remained largely stable. Investors who stayed invested recovered fully within 18 months and went on to generate significant gains. This was a landmark moment that validated the "stay invested" philosophy at scale.

Understanding the Current Global Environment

To appreciate the significance of this shift, it is important to understand the broader economic backdrop. The global economy in 2026 faces several challenges simultaneously:

- Rising Geopolitical Tensions: Conflicts impact energy prices, trade routes, supply chains, and commodity markets. Higher uncertainty historically triggered widespread investor anxiety and outflows from equity markets.

- Inflation Concerns: When inflation rises, consumer purchasing power declines, central banks may increase interest rates, borrowing becomes expensive, and economic growth can slow.

- Interest Rate Uncertainty: Central banks must balance controlling inflation, supporting economic growth, and maintaining financial stability.

- Economic Slowdown Fears: Businesses face higher costs, supply chain challenges, increased competition, and changing consumer demand.

🔑 Why This Context Matters

Despite all of the above headwinds, India's monthly SIP inflows grew from approximately ₹8,500 Cr in 2020 to over ₹26,600 Cr in December 2024 — more than 3x growth in 4 years. This happened during one of the most uncertain global economic periods in recent memory.

The Emergence of the Unbreakable SIP Investor

A new generation of investors is challenging traditional behaviors. These investors understand several important truths:

Truth #1: Volatility Is Normal

Markets do not move in straight lines. Corrections are not exceptions — they are expected components of long-term investing. The Nifty 50 has experienced a correction of 10%+ in most calendar years, yet still delivered ~13% CAGR over the last 20 years.

Truth #2: Time Matters More Than Timing

The duration of investment often has a greater impact on wealth creation than perfect entry points. SIPs structurally close the gap between what funds deliver and what investors actually earn.

Truth #3: Every Market Crash Eventually Ends

History shows that markets have repeatedly recovered from recessions, wars, and financial crises. The Global Financial Crisis (2008) took ~28 months to recover, while the COVID-19 crash recovered in just ~18 months.

Data Snapshot: The New Investor Mindset

| Old Investor Mindset | New SIP Investor Mindset |

|---|---|

| Fear market declines | Accept market declines as buying opportunities |

| Stop investing during crashes | Continue investing during crashes |

| Focus on short-term returns | Focus on long-term goals |

| Attempt market timing | Follow disciplined, automated investing |

| React to news headlines | Follow a written investment plan |

The Mechanics Behind SIP Success and Compounding

A Systematic Investment Plan (SIP) allows investors to invest a fixed amount regularly — regardless of market conditions. Most investors struggle not because of poor investment products but because of inconsistent behavior. SIPs solve this by automating discipline.

The Mathematics of Wealth Creation (Example: ₹5,000 Monthly SIP @ 12% p.a.)

| Investment Period | Total Invested | Estimated Corpus @12% |

|---|---|---|

| 5 Years | ₹3,00,000 | ₹4,12,000 |

| 10 Years | ₹6,00,000 | ₹11,60,000 |

| 15 Years | ₹9,00,000 | ₹25,20,000 |

| 20 Years | ₹12,00,000 | ₹49,90,000 |

| 25 Years | ₹15,00,000 | ₹94,80,000 |

By year 25, ₹15 Lakhs invested becomes ₹94.8 Lakhs. This is compounding in action. As Warren Buffett says, "Do not save what is left after spending; instead spend what is left after saving."

Start your transformational decade today. Consistency is the key.

Calculate Compounding Growth on VittarthiRupee Cost Averaging: The Hidden Advantage

One of the biggest structural advantages of SIPs is Rupee Cost Averaging (RCA). When markets fall, your fixed monthly amount buys more units. When markets rise, you buy fewer. Over time, this lowers your average cost per unit.

| Month | NAV | Investment | Units Purchased |

|---|---|---|---|

| January | ₹100 | ₹10,000 | 100.00 |

| February (Dip) | ₹80 | ₹10,000 | 125.00 |

| March (Further Dip) | ₹70 | ₹10,000 | 142.85 |

| April (Recovery) | ₹90 | ₹10,000 | 111.11 |

| May (New High) | ₹110 | ₹10,000 | 90.90 |

An investor who panicked and stopped SIPs in March would have missed buying 142 units at low prices — units that were worth significantly more by May. Stopping a SIP during a crash is often the most expensive financial mistake an investor makes.

The Rise of Flexi-Cap Funds

One of the biggest beneficiaries of changing investor behavior has been Flexi-Cap Funds. These funds can invest across Large-Cap, Mid-Cap, and Small-Cap stocks without strict allocation limits. Fund managers dynamically adjust exposure based on market conditions, combining stability, growth, and aggressive opportunities into one portfolio.

By delegating allocation decisions to professional fund managers, investors experience lower decision fatigue. This psychological comfort reduces the urge to exit during volatility — which is often the primary driver of long-term underperformance.

Behavioral Finance: The Hidden Driver Behind Investment Success

Investment success is often determined more by behavior than by product selection. The biggest threats to long-term wealth creation are usually Fear, Greed, Impatience, Overconfidence, and Panic selling.

Mistake 1: Panic Selling

During corrections, investors sell fearing further losses. Markets frequently recover before they re-enter, resulting in "sell low, buy back higher."

Mistake 2: Chasing Performance

Investors pile into funds after strong performance. By the time the majority enters, valuations may already be elevated.

Building a Wealth Creation Framework

- Establish Emergency Savings: Build 6–12 months of expenses in a liquid account.

- Define Financial Goals: Map SIPs to specific goals (Retirement, Home ownership).

- Choose Appropriate Asset Allocation: Balance across Equity, Debt, and Gold.

- Automate with SIPs: Remove emotional interference.

- Remain Invested: Time in the market matters more than timing the market.

Final Conclusion: The New Era of Investing

The rise of the Unbreakable SIP Investor represents one of the most important behavioral shifts in modern personal finance. For decades, retail investors responded to uncertainty with fear. Today, a growing number of investors are embracing Discipline over emotion, Process over prediction, Patience over panic, and Long-term wealth creation over short-term speculation.

The success of SIP investing is not based on predicting the future. It is based on accepting uncertainty while remaining committed to long-term goals. Successful investors are not necessarily those who predict every market movement correctly. They are the ones who remain invested long enough for discipline, compounding, and time to work together.

Markets will always fluctuate. Discipline does not have to.

Frequently Asked Questions (FAQs)

What is an SIP?

A Systematic Investment Plan allows investors to invest fixed amounts regularly into mutual funds, leveraging Rupee Cost Averaging.

Is SIP investing risk-free?

No. SIPs reduce timing risk but do not eliminate market risk. However, long-term SIPs in diversified equity funds have historically generated superior returns.

Can SIPs generate wealth during market declines?

Yes. Market declines allow investors to purchase more units at lower prices. This significantly enhances long-term returns when markets recover.

What are Flexi-Cap Funds?

Flexi-Cap Funds invest across large, mid, and small-cap stocks without strict allocation limits, offering flexibility and professional risk management during uncertain times.

Tags & Keywords: Unbreakable SIP Investor, Wealth Creation Case Study, Rupee Cost Averaging, Flexi-Cap Funds, Behavioral Finance in Investing, Vittarthi Financial Research, Market Volatility Strategy.